1. Credit Cards – I realize that credit cards are one way many people accrue debt. I make money with mine. Advanced Warning – applying for a credit card is a hard pull on your credit report. Hard inquiries will temporarily reduce your credit rating. It is not wise to apply for many credit cards at the same time. You also shouldn’t apply for new credit cards if you know you are going to apply for a house loan in the next few months. Many people have strong enough credit that it doesn’t matter, but these are typically best practices.

2 Ways To Make Money With Credit Cards

Signup Bonuses

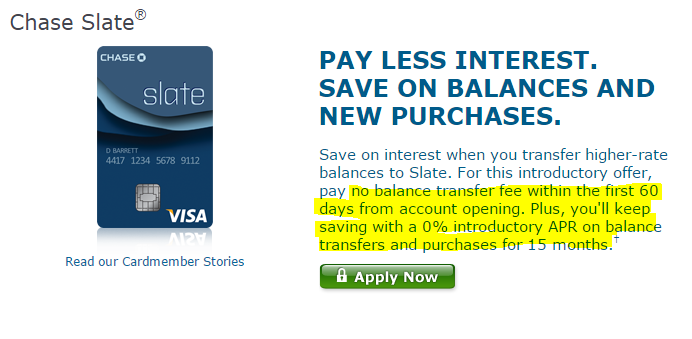

If you have already accumulated debt, you would be wise to search for a credit card with 0% financing on balance transfers (typically 6-18 months) and no transfer fee. The latter part is important because most credit cards offering 0% financing typically charge a transfer fee around 3%-5%. The Chase Slate card is the most common credit card offered with a 0% balance transfer fee within the first 60 days and 0% financing for 15 months. The other biggie with the Chase Slate card is it has no annual fee. If you are interested in this option, you might also check with Discover. Most of their offers involve a transfer fee, but I have had a fee sent to me with no fee and a 0% introductory APR.

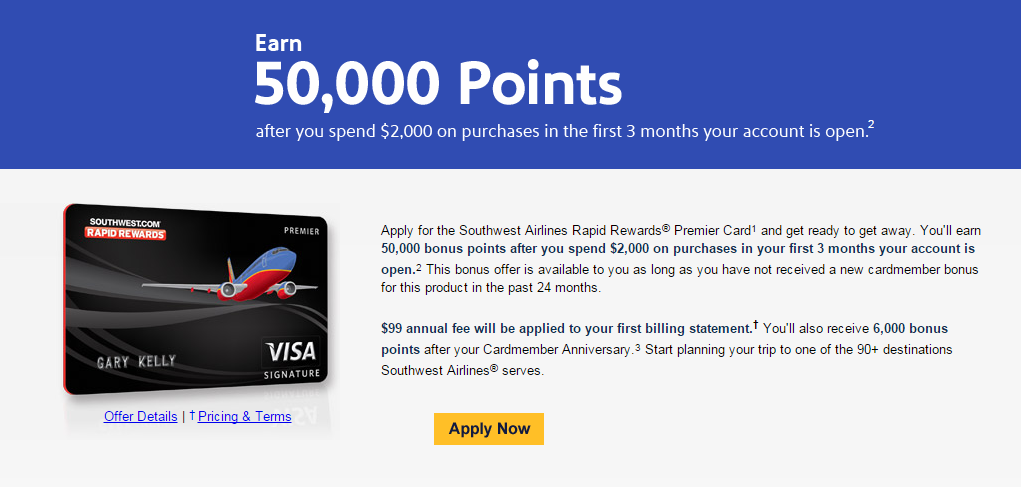

If you don’t have credit card debt you need to refinance, the Southwest Airlines card by Chase currently has one of the best signup bonuses. You will receive 50,000 bonus miles (roughly $700 worth of flights) after spending $2000 in the first three months. There is a $99 annual fee that is not waived. Since there is an annual fee, I recommend using this as a churn card (you can currently only receive this bonus every 24 months). The standard benefits are not good enough to continue using the card after earning the signup bonus.

Cashback On Purchases

I typically earn about $1000 dollars a year in cashback by strategically using my credit cards. A lot of my earnings accrue from an old Citi Forward card that gives me 5% back (in thank you points) on restaurants and Amazon (book stores). Unfortunately, the newer terms are not as generous. It was intended as a college card, but obviously didn’t have the intended results for the Citi bottom line.

Current Cards That Rock

- Chase Freedom & Discover – these cards are almost the same card from different companies. They both have no annual fees and offer 5% cashback on quarterly rotating categories. If you are good keeping track of the categories, you might as well get both cards. Chase Freedom frequently has a $200 signup bonus after just $500 worth of purchases in the first three months.

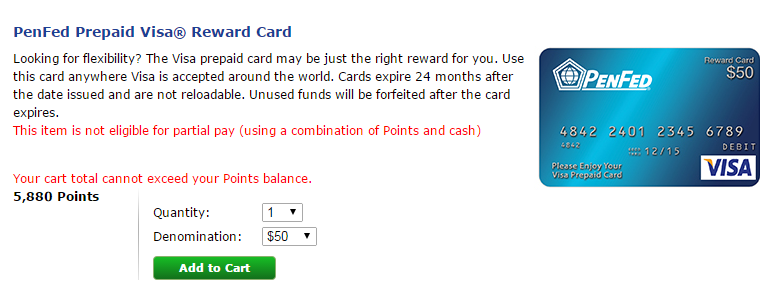

- Penfed – this card is from the Pentagon Federal Credit Union. They are remarkably good all around financial institution. I found them originally because they had the lowest rates on used auto loans. Their credit card gives 5 points for gas purchases and 3 points for grocery stores. The rates used to be 5% and 3%, but they switched to a slightly less lucrative point system about a year and a half ago. The switch made the points a little less than 20% less valuable. Said another way, you will actually earn a little over 4% cashback on gas purchases. It is worth noting you will need to make a couple dollar donation to the American Red Cross to qualify to join Penfed if you are not part of the normal network. It’s one of those odd legacy credit union rules.

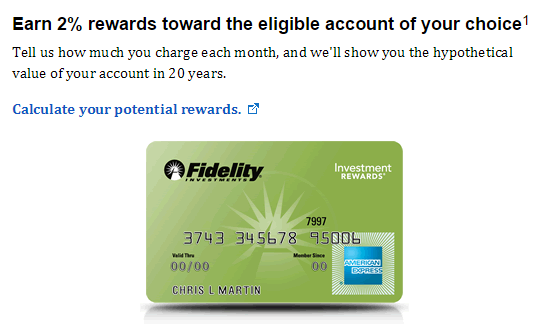

- Fidelity Amex – This is the only card I’ve mentioned that I don’t personally have. Why don’t I have it? I have a Bank of America card that gives me 2.5% cashback on all purchases when I collect more than $300 in cash rewards. Since I have never seen the BOA deal offered to the general public, the Fidelity Amex card is my recommended card for general day-to-day cashback. AMEX cards typically come with an annual fee. This card does not. The other component I love is that the earnings can be deposited into your IRA. This is a tremendous way to turn a little money now into a lot of money during retirement.

2. Cashback Websites – In the affiliate industry cashback websites are referred to as loyalty sites. Discover Deals uses the loyalty site model. My favorite cashback websites are MrRebates and Ebates. Combine these cashback websites with deals from Slickdeals, Google Shopping and FatWallet to save more money. Be careful with Slickdeals and FatWallet. Many people go on a shopping binge when they first become part of the community. Google Shopping is the best and most widely used comparison shopping engine (CSE). The advantage is that many merchants put slightly lower prices on Google Shopping because they know they are competing with the masses. We actually used a source code embedded in the end of the tracking link that would set a cookie, resulting in 5% lower prices than if you hadn’t gone through Google Shopping. Pricewatch was the first CSE I used in the mid 90s. Unfortunately, they never evolved beyond computer parts and many bad merchants started gaming the system. People still game Google Shopping. It is important to stick to stores that are rated well. FatWallet merged with Ebates a few years back, but Ebates still tends to offer higher cashback rates. This screenshot will give a slight indication as to how long and how frequently I use MrRebates.

3. Pay for Your Car Insurance 12 Months at a Time – many people don’t realize car insurance policies can be purchased in 12 month cycles. They think you can only buy the policy 6 months at a time. I have used this strategy with both Kemper Preferred and Progressive. If you think about it, a tremendous amount of what we pay for insurance is marketing spend. Insurance companies help create this problem by dicking over loyal customers. It is statistically proven that people who don’t switch car insurance companies end up paying more. The caveat here is you don’t want to lock in a rate for 12 months if you are about to experience a dramatic decline. Examples would be right before you turn 25 or when a wreck is soon to drop off your record. It would also be silly to pay for a 12 month insurance policy with a credit card with a balance. Think of it like an airline hedging their bets by buying oil an advance. If they think the rate is going to drop, they might lock in a relatively small amount. If they think oil prices are going to increase, they will lock in the rate as long as they possibly can.

4. Haggle with the Cable Company – recurring bills are the bane of my existence. Even a little increase adds up to a substantial amount when you multiply it by 12x or 365x. I recently saw that my Time Warner internet bill had gone from a manageable $45 a month an unsustainable $70 per month. BTW, that is the exact phrasing I used when speaking with the Time Warner rep – this bill is unsustainable. The representative said that he needed to investigate. Within a couple minutes, he said that he added a 12 month discount rate of $39.99 to my bill. This was about the fifth time I had used this exact same strategy. I only encountered one woman who would not budge. If you happen to get that sad CSR, hang up and call again. The next person will hook you up. You need to put on your sales person hat in these situations. Be nice but be firm. Other strategies are to mention the introductory rates you have received from ATT or whatever competitor is in your area. Fortunately for us in Austin, this is about to become a moot point with the arrival of Google Fiber. I am only paying Google an initial fee of $300 spread over 12 months to add fiber to my house. Then they are going to give me Internet (5Mbps down and 1 Mbps up) free for the next six years. That is going to be a real win.

![]()

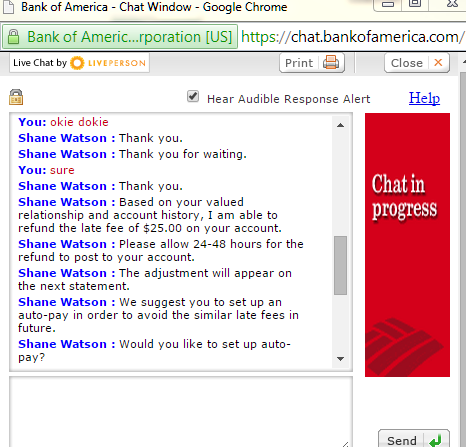

5. Ask a Bank to Waive Fees – I must make another confession here. I don’t always pay my bills on time. This has never been due to a lack of funds. It results from poor planning. Anyway, if you have a credit card and you were late paying, ask them to waive the fee. You can also use this strategy for over draft fees. Those were more of a problem several years ago when banks would purposely approve transactions to gain the $35 fee or reorder purchases to make clients accumulate additional late fees. This strategy again requires using your salesman hat. Be nice to the rep and emphasize the fact that you are a good customer.

Note the banking representative asked me to setup auto-pay. I promptly took him up on this offer. I don’t pay the full balance through auto-pay, but I make sure that at least the minimum is covered to ensure I do not incur late charges. Discover setup this program for me with no work on my part. Bank of America required a somewhat tedious process, but it took less than fifteen minutes in the end.

6. Use an Off Brand Phone Provider – By off brand phone provider, I mean Cricket, Virgin Mobile, Boost Mobile, Metro PCS, etc. My co-worker said, “don’t only drug dealers use that” when I said I had switched to Cricket Wireless. The reality is that all the sub-brands use the exact same service as the larger brands.

- Cricket – AT&T Owned Company

- Boost / Virgin – Sprint

- Metro PCS – they are actually owned by T-Mobile. They are purely using a different marketing strategy.

- Straight Talk – weird mix of Verizon, ATT, and Sprint

If you do not believe what I just said or say their must be some disadvantage of the sub-brand services, marketing works well on you my friend. I don’t mean that to be a condescending statement. Marketing works well on me too. The only difference is that I have seen too many cases where people are able to charge 5x or 10x more on a product simply because they advertise it more.

Name brands (ATT, Sprint, Verizon, T-Mobile) provide great deals to people on family plans. They offer horrendous rates to people who are simply paying for themselves. The main advantage of major brand cell phone providers used to be that they would give you a shiny new iPhone every 2 years. While that is still true, you can buy a similar phone out of pocket and with no contract for just a couple hundred. The math doesn’t work out anymore with the name brand carriers. The same providers are providing the service in the back end.

I sincerely hope you take these strategies to heart. I am not bullshitting. I have used every single one of these methods and they will save you a substantial amount of money in the long run.

6/14/15 Update about Cricket

Since AT&T owns Cricket and merged legacy customers onto their network, AT&T branded phones will work on Cricket. These phones do not have to be unlocked to work. Here are the steps to make the AT&T phone work.

1. Call Cricket at 1-800-CRICKET to add the IMEI or add it in your online account settings.

2. Take the SIM card from your old device or have Cricket send you a new one. Once the sim is added the port will work.

Leave a Reply